Private Equity M&A Activity Better than Expected in Q1

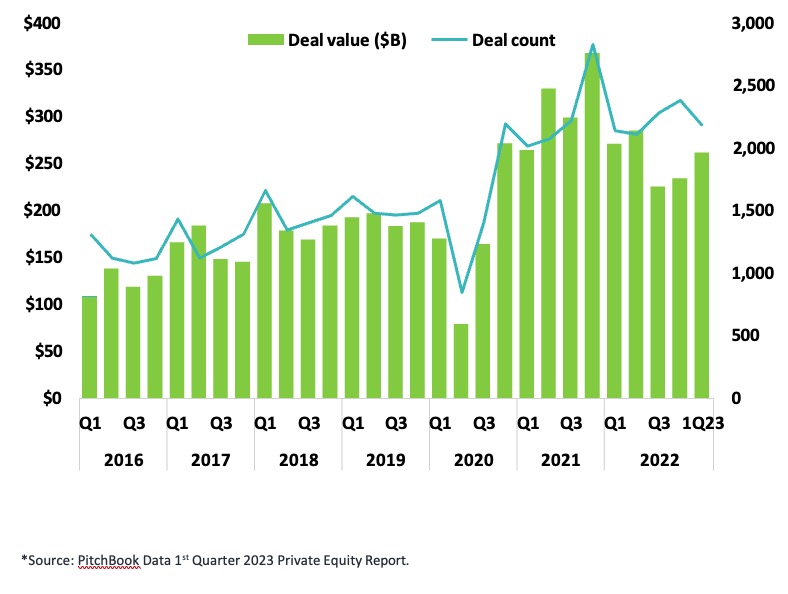

According to PitchBook Data, 1Q 2023 U.S. private equity M&A deal count dropped on a sequential basis by 8% vs. 4Q 2022 but thanks to some large deals, value was up 11% on a sequential basis. On a year over year basis, 1Q 2023 deal count was down 1% as compared to 1Q 2022 but deal value was down 4% indicating either a smaller average deal size or lower valuations or a combination of both. Given the current environment, however, we would expect to see a drop in activity in 2Q 2023 although we believe this could represent the trough in activity for the year.

U.S. Private Equity Activity – Annual ($Bns)*

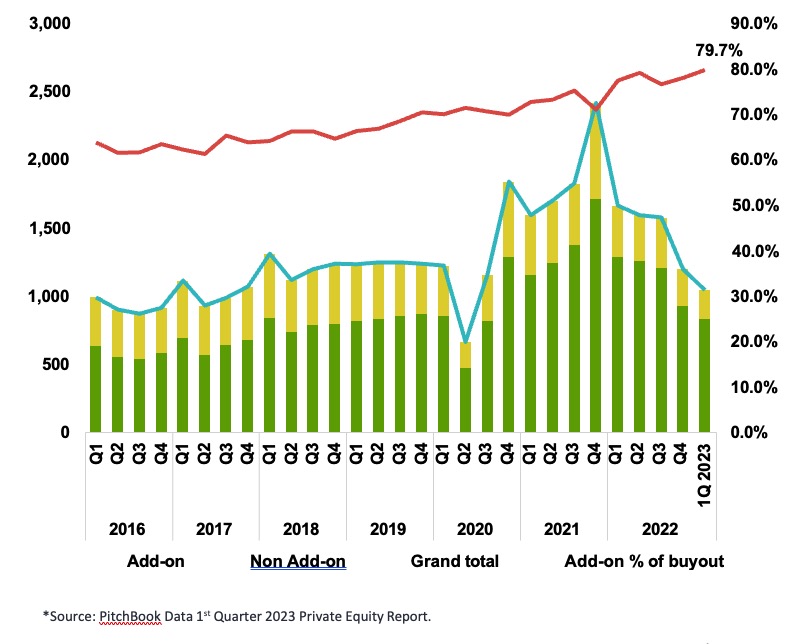

Add-On Activity Further Demonstrates Resiliency of LMM

According to PitchBook Data, the percentage of private equity deals representing add-on acquisitions by existing portfolio companies as compared to acquisitions of platform companies accelerated to a record 80% in 1Q 2023. While the primary cause is likely the continued benefit of multiple arbitrage, this also demonstrates the relative strength of the lower middle market as compared to the core and upper middle market segments where companies are much more impacted by higher interest rates, tightening credit markets and other macroeconomic factors.

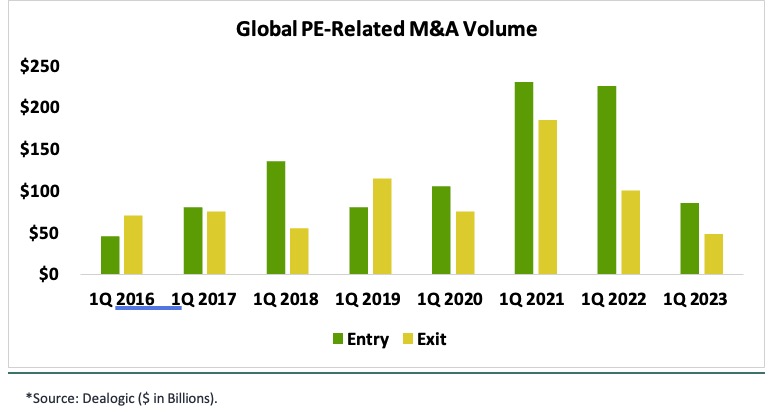

Private Equity Exits Slow Dramatically in 1Q 2023

According to Dealogic, private equity exits slowed down dramatically beginning in 2022 and into Q1 2023 as the impact of rising interest rates and unsettled debt markets has taken its toll on M&A activity. Just as the insider trading activity of publicly traded companies can foretell company performance three to six months out, the selling activity or lack thereof of private equity firms says a lot about their outlook. On the flip side however at a recent ACG Los Angeles private equity panel, the general consensus was the bottom will be seen in Q2 and the rebound will begin in Q3 when a number of portfolio companies are put on the market.

*Source: Dealogic ($ in Billions).

Noticeable Uptick in Corporate Carveouts

PE firms have seen an increase in deals from public companies selling non-core operations. The % of all PE deals that represent carveouts bottomed at 5.1% in Q4 2021 and increased to 7.6% in Q4 2022. While there was a dip in Q1 2023, our research indicates the upward trend has continued noticeably in Q2 2023.

Credit Markets Tighter with Rates Stable at High Levels

Lenders continue to be very selective in supporting leveraged buyouts, exacerbating the slowdown in private equity M&A activity. Many banks are totally out of the market while others require ancillary business such as deposits, foreign exchange and credit card processing to even consider a new deal. If you can get it all, the cost of bank debt (currently 8% – 9%) has literally doubled in the past year since the base rate, either prime or SOFR, has gone up 10x and spreads have widened. Also, the cost of debt from credit funds has gone up by about 50% even while leverage levels have come down (now 12% to 15% for leverage up to 4x vs. 8% to 10% for leverage up to 5.5x). Sounds similar to food companies who charge more while reducing package sizes!

Large, strong credits who have been shunned by the banks recently are increasingly going to credit funds and BDCs. As a result, these alternative lenders have been seeing much higher quality deal flow leaving smaller and marginal credits by the wayside.

Bottom Line: Good Deals are Still Getting Done

Companies with strong financials (stable and growing revenues and margins) are still able to sell at attractive multiples especially in the following sectors:

- Food

- Software

- Tech-Enabled Services

- Healthcare/Medical Products & Services

- Niche Manufacturing

- Industrial Technology

- Luxury Consumer Goods

- Franchising

- Home Services

- Critical Infrastructure Services

- Repair & Maintenance