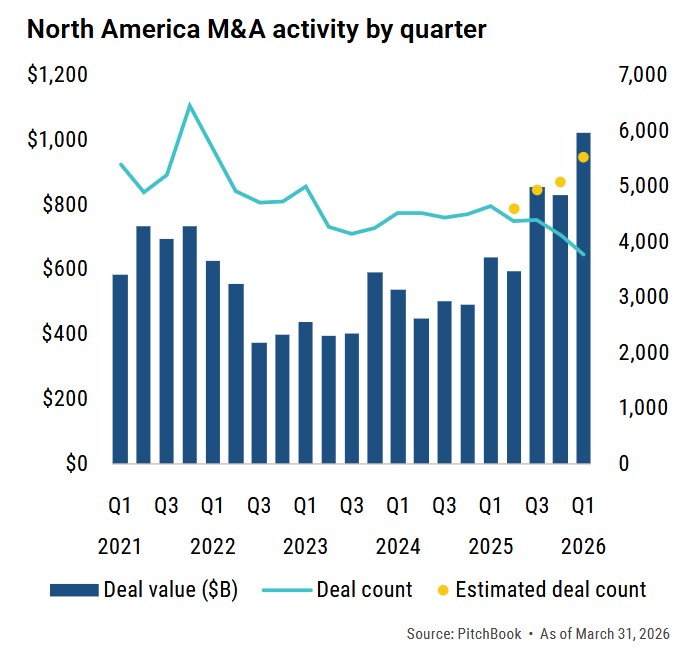

M&A Begins to Rebound in 1Q24 Albeit Slowly

According to Pitchbook, in the first quarter of 2024 (1Q24) North America M&A activity was solid despite the persistently challenging dealmaking conditions. Total M&A value for 1Q24 of $464.1 billion was 9.7% higher on a year-over-year basis as compared to 1Q23. Deal volume (number of deals) came in at 4,204 in 1Q24, which represented a 2.0% decline vs. 1Q23.

Rebound in Private Equity Activity Delayed

The value of private equity acquisitions in 1Q24 was 22.7% lower on a year-over-year basis than 1Q23, however deal count was up 6.4%.

At a time of rising rates and tightening credit conditions, strategic buyers tend to have an upper hand over financial buyers. This has been the case for about the past 18 months and this trend continued in 1Q24. This explains why overall North American M&A has bounced back quicker than private equity activity.

Lower Mid-Market Valuations Continue to Bounce Back

According to GF Data, PE Lower Mid-Market ($10-$250MM in value) multiples bounced back to 7.5x in 1Q24 after dropping below 7x on a quarterly basis twice in the past five quarters.

Market Outlook Continues to Look Very Favorable

Looking ahead, the potential for lower rates later beginning later in 2024 and into 2025, contingent on moderating inflation data, instills optimism for a potential

rebound in deal activity albeit not quite as soon as most had been hoping. M&A activity was down for two consecutive years in 2022 and 2023. This does not happen very often and when it does, the following year is almost always up. The last two times this happened were 2001 – 2002 and 2007 – 2008 and both times the following year was up.

The following comments by a prominent publicly traded BDC made during a 1Q24 earnings call provide an accurate depiction of the current state of the market:

- Banks are more active again and this is good for all market participants as the increased availability of capital typically brings out more M&A and adds confidence to companies seeking financing for transactions.

- The firming of the credit markets, the aging of significant amounts of private equity dry powder, and the continued pressures from LPs to return capital are all factors that support higher levels of activity.

- We’re seeing signs of a pickup in transaction activity as evidenced by the $1.2 billion of commitments we’ve closed in the second quarter to date.