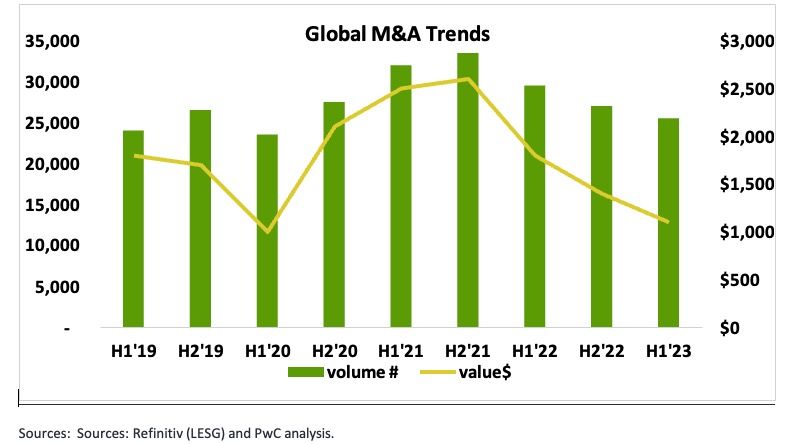

No Surprise – Global M&A Down Significantly in 1H23

According to PwC, the value of global M&A deals in the first half of 2023 (1H23) was down 39% vs. 1H22 and down 56% vs. 1H21. Deal volume was down 14% in 1H23 vs. 1H22 and down 20% vs. 1H21.

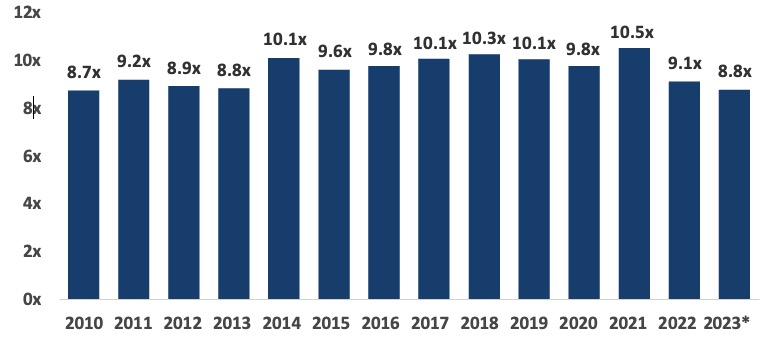

Valuation Multiples Have Corrected

According to PitchBook, EBITDA multiples in North America and Europe in 1Q 2023 decreased by 16% from the peak in 2021 and back to levels not seen since 2013.

*Source: PitchBook Data 1Q 2023 Global M&A Report—N. America & Europe (All Industries)

According to Reuters, 2Q23 M&A volume in the U.S. declined by 30% year-over- year to $318.4 billion, while Europe and Asia Pacific volumes shrank 49% and 24% respectively.

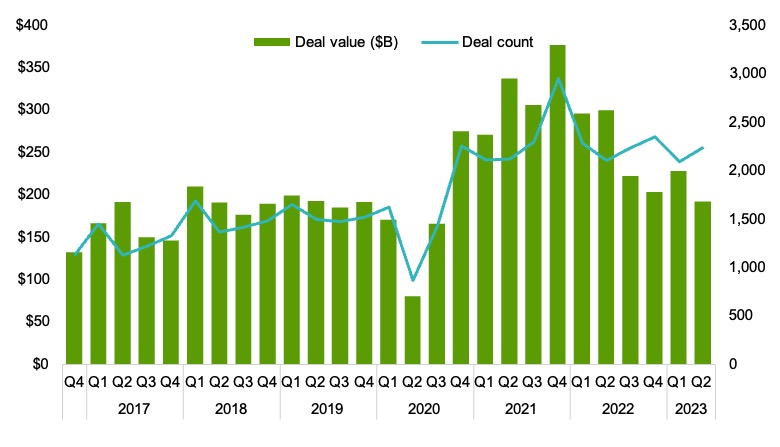

Private Equity Activity Hurt by Credit Markets

According to PitchBook 2Q23 Private Equity M&A activity was mixed with value down 36% year-over-year vs 2Q22 but volume up 7%. Compared to the peak in 4Q21, 2Q23 value was down 49% while volume was down 24%.

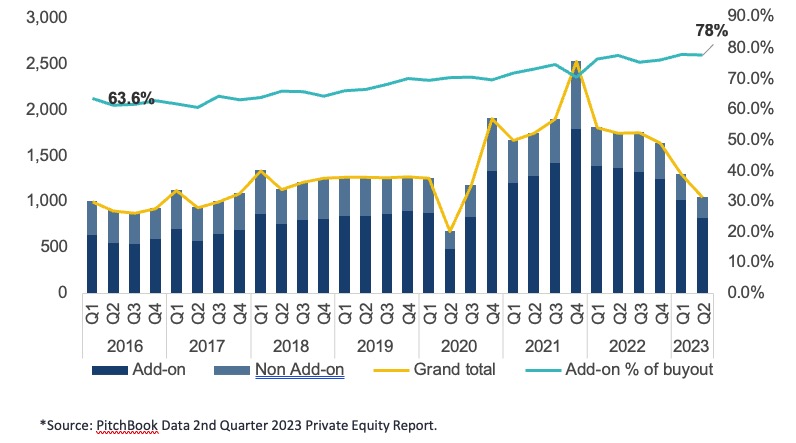

U.S. Private Equity Activity – Annual ($Bns)*

Source: PitchBook Data 2nd Quarter 2023 Private Equity Report.

The slowdown is more pronounced when looking at global deal activity. According to Dealogic, so far this year, private equity-led buyout volumes globally have slumped 59% year-on-year to $196.66 billion. In the second quarter, sponsor-led buyout volumes fell 56% to $110.55 billion.

One major cause for this decline is the contraction in credit markets and higher cost of capital. We also are observing a number of deals being intentionally delayed coming to market – some because their financial performance has been inconsistent while others are hoping valuations recover at least somewhat later this year or early next year. At the same time, we are seeing gradual signs of a recovery in deal activity as more companies have maintained strong financial performance and are ready to go to market sooner than later.

Add-On Activity Further Demonstrates Resiliency of LMM

According to PitchBook, the percentage of private equity deals representing add- on acquisitions by existing portfolio companies as compared to acquisitions of platform companies accelerated to 78% in 2Q 2023. While the primary cause is likely the continued benefit of multiple arbitrage, this also demonstrates the relative strength of the lower middle market as compared to the core and upper middle market segments where companies are much more impacted by higher interest rates, tightening credit markets and other macroeconomic factors.

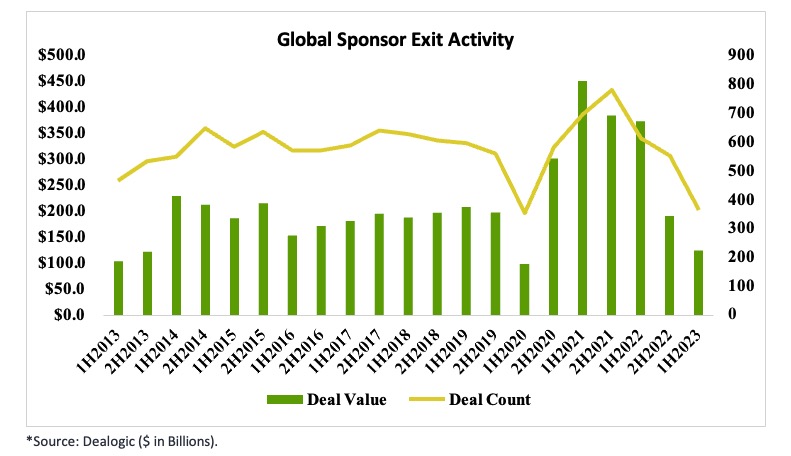

Private Equity Exits Slow Dramatically in 1H2023

According to Dealogic, global private equity exits slowed down dramatically beginning in 2022 and into 1H23 as the impact of rising interest rates and unsettled debt markets has taken its toll on M&A activity.

Noticeable Uptick in Corporate Carveouts

PE firms have seen an increase in deals from public companies selling non-core operations. The % of all PE deals that represent carveouts bottomed at 5.0% in Q4 2021 and increased to 7.8% in Q2 2023.

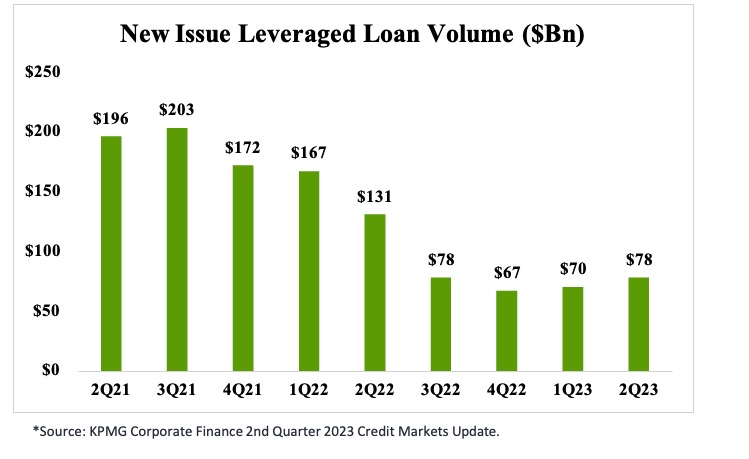

Credit Markets Remain Tight

According to KPMG, new issue leveraged loan volume in 2Q23 reached $77.9 billion, down 41% from the $131.3 billion in volume in 2Q22 but the highest in the past three quarters.

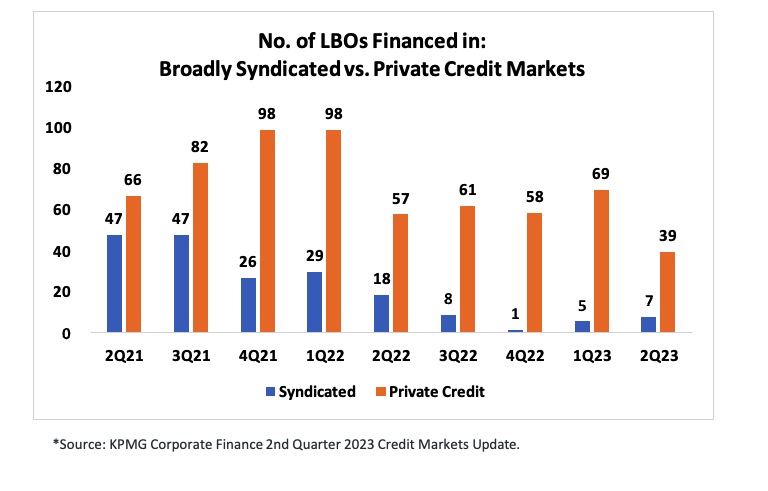

Private credit funds continue to dominate the leveraged buyout market over broadly syndicated loans. Borrowers have been willing to pay the higher cost of private credit in exchange for a higher certainty of close.

Bottom Line: Good Deals are Still Getting Done

Companies with strong financials (stable and growing revenues and margins) are still able to sell at attractive multiples (albeit in most cases below the peak levels seen in late 2021) especially in the following sectors:

- Food

- Software

- Tech-Enabled Services

- Transportation & Logistics

- Healthcare/Medical Products & Services

- Niche Manufacturing & Distribution

- Luxury Consumer Goods

- Franchising

- Home Services

- Critical Infrastructure Services

- Repair & Maintenance