M&A 2nd Half 2023 Rebound Deferred Until 1st Half 2024

According to S&P, the number of M&A deals in North America in 3Q23 (3,640) fell 30% year-over-year from 3Q22 and was down 15% on a sequential basis vs. 2023.

Factors contributing to the decline include:

- a decline in financial performance in several industry sectors so far this year as compared to last year (at least partially due to the impact of inflation on customer demand whether B2C or B2B);

- tighter credit conditions; and

- higher for longer interest rates.

As a result, the rebound in deal activity many were expecting to see in the second half of this year has been postponed until the first half of 2024. There is a quite a backlog of M&A and public market deals building up and assuming the Fed does indeed stop raising rates soon, we should see a nice rebound in the first quarter and if rates start coming back down at least a little bit, 2024 should be a very strong year for private and public market deal activity (nothing like the frenzy in 2021 but better than this year and maybe better than last year). In the past few months, most bankers like us have observed an increase in pitch activity and have signed up new sell-side engagements which also bodes well for 2024.

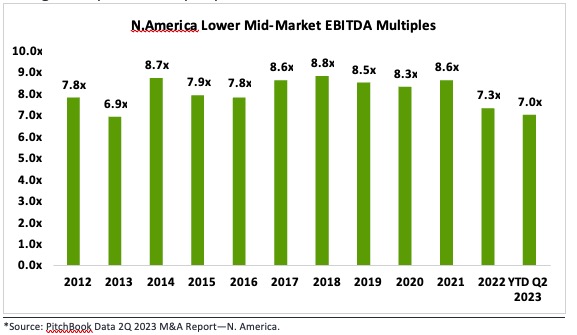

Valuation Multiples Have Corrected

According to PitchBook, North American lower middle market (under $200mm) valuation multiples dropped in the first half of 2023 to 7.0x, the lowest level in 10 years. Due to a scarcity of high-quality deal flow, however, companies with strong financial performance are still getting significant premiums to average market multiples. At the same time, smaller companies at the lower end of the lower middle market and those with uneven financial performance are seeing below average multiples or have postponed transactions.

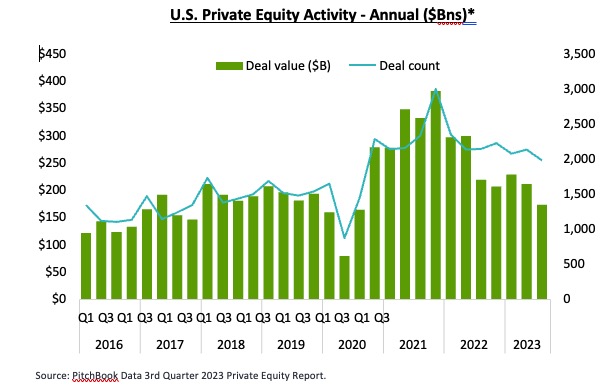

Private Equity Activity Especially Hurt by Credit Markets

According to PitchBook, 3Q23 Private Equity M&A activity was mixed with value down 25% year-over-year vs 2Q22 but volume (no. of deals) down only 7%.

One major cause for this decline is the contraction in credit markets and higher cost of capital. We also are observing a number of deals being intentionally delayed coming to market – some because their financial performance has been inconsistent while others are hoping valuations recover at least somewhat next year. At the same time, we are seeing gradual signs of a recovery in deal activity with more pitches and new engagements for deals to bring to market in 2024.

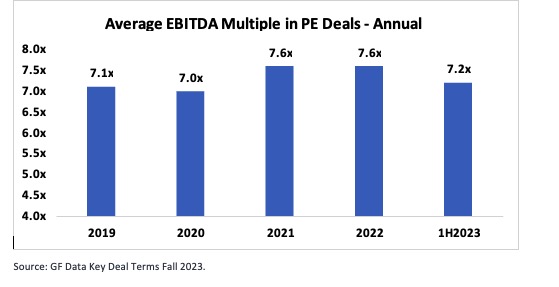

Private Equity Acquisition Valuation Multiples Decline

According to GF Data (a division of ACG), multiples paid by private equity firms in the lower middle market ($10mm – $250mm in deal value) retreated in the first half of this year to a more normal (pre-Covid) level (7.2x).

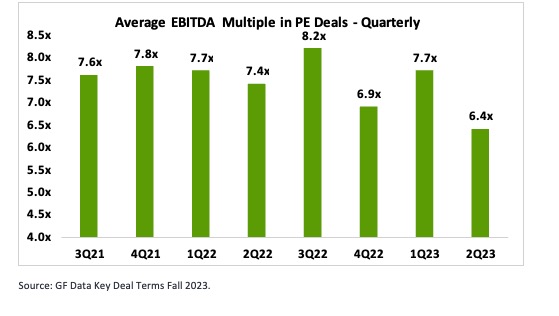

The decline in private equity acquisition multiples is much more pronounced when viewed on a quarterly basis. The average multiple paid dropped to 6.4x in 2Q23.

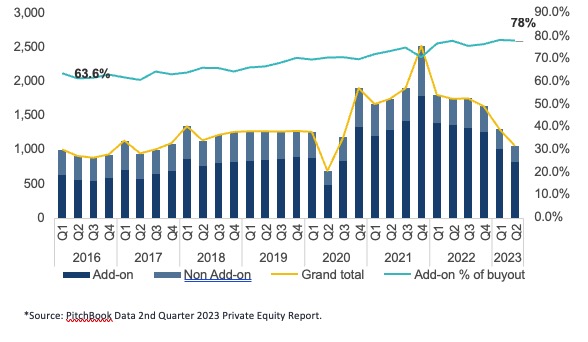

Add-On Activity Further Demonstrates Resiliency of LMM

According to PitchBook, the percentage of private equity deals representing add- on acquisitions by existing portfolio companies as compared to acquisitions of platform companies accelerated to 78% in 2Q 2023. While the primary cause is likely the continued benefit of multiple arbitrage, this also demonstrates the relative strength of the lower middle market as compared to the core and upper middle market segments where companies are much more impacted by higher interest rates, tightening credit markets and other macroeconomic factors.

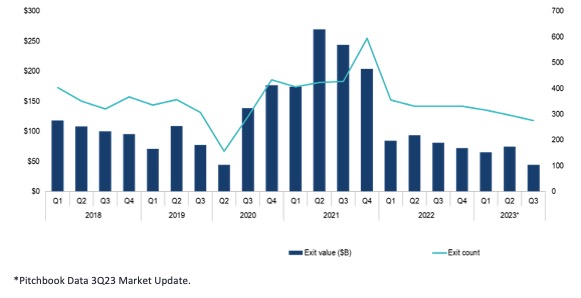

Private Equity Exits Slow Dramatically in 2023

According to Pitchbook, U.S. private equity exits slowed down dramatically beginning in 2022 and into 1H23 as the impact of rising interest rates and unsettled debt markets has taken its toll on M&A activity. Year to date 3Q23 exits were down by 13% vs. last year and down by 29% as compared to the first three quarters of 2021. This year’s exits so far are also below levels since in the same periods in 2018 (-17%) and 2019 (-11%).

Noticeable Uptick in Corporate Carveouts

PE firms have seen an increase in deals from public companies selling non-core operations. The % of all PE deals that represent carveouts bottomed at 5.0% in Q4 2021 and increased to 7.0% in 3Q23.

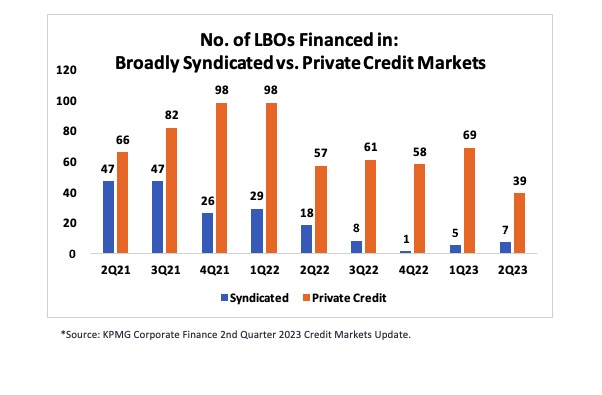

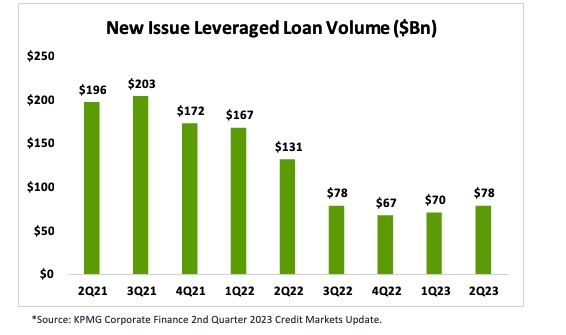

Credit Markets Remain Tight

According to KPMG, new issue leveraged loan volume in 2Q23 reached $77.9 billion, down 41% from the $131.3 billion in volume in 2Q22 but the highest in the past three quarters.

Private credit funds continue to dominate the leveraged buyout market over broadly syndicated loans. Borrowers have been willing to pay the higher cost of private credit in exchange for a higher certainty of close.