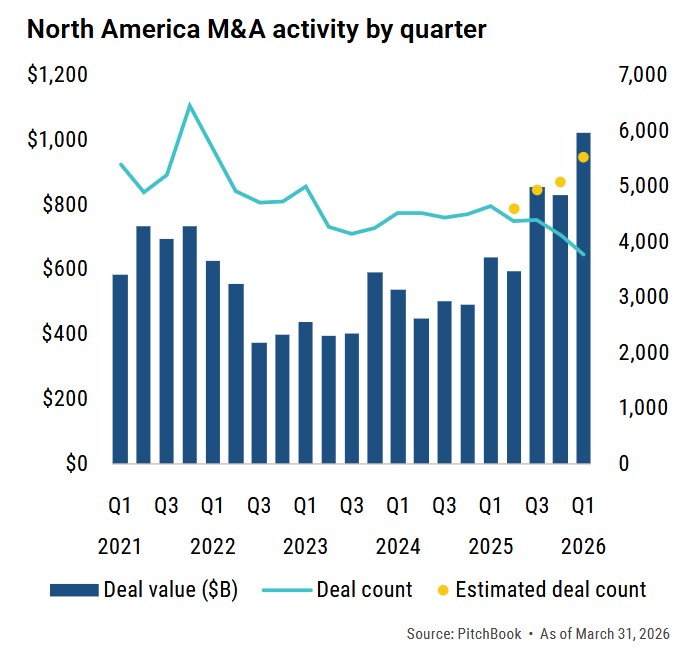

U.S. Private Equity M&A Activity in 2022

According to PitchBook Data, total private equity M&A volume decreased in 2022 by only 2.5% to 8,897 deals but the value of private equity activity declined by 19.5% to $1.0 trillion.

Activity in Q4 2022 dropped by 23.4% in terms of deal count and by 41.8% in terms of value on a year over year basis as compared to Q4 2021.

*Source: PitchBook Data 4nd Quarter 2022 Private Equity Report.

The higher relative drop in value is a function of both lower valuation multiples and lower average deal size. According to GF Data, Private Equity valuations retreated in Q4 to an average multiple of 6.8x according to GF Data’s recently released Q4 M&A report on $10-250mm PE sponsored transactions down from 7.6x in Q4 2021. Deal count also remained soft—off nearly 60% from the fourth quarter of 2021.

Add-On Activity Further Demonstrates Resiliency of LMM

According to PitchBook Data, the percentage of private equity deals representing add-on acquisitions by existing portfolio companies as compared to acquisitions of platform companies accelerated to a record 80% in 4Q 2022. While the primary cause is likely the continued benefit of multiple arbitrage, this also demonstrates the relative strength of the lower middle market as compared to the core and upper middle market segments where companies are much more impacted by higher interest rates, tightening credit markets and other macroeconomic factors.

At the same time, the median value of PE add-on acquisitions fell back to $51MM in 2022 after spiking to $75MM in 2021.

Credit Markets Tighter With Rates Increasing

Buyers who rely aggressively on leverage (like many if not most PE buyers) have been hit with a double whammy of tighter credit markets and higher rates.

- Lenders are more discerning with cyclical industries and seek lower loan-to- value levels,

- Lenders reprice existing financings for add-on acquisitions and other consent requests,

- Junior debt is back in favor as first lien lenders retrench on leverage levels,

- To attract lenders, borrowers are having to offer high spreads; in combination with rising interest rates, debt service obligations are growing meaningfully, resulting in a compression in leverage multiples, and

- Although aggregate borrower financial performance is slowing, relatively low default rates to date have sustained the private credit markets, demonstrating the strength and stability of the asset class.

The following chart demonstrates the impact of the rapid increase in rates and tightening of credit along with the related drop in valuations. Observations:

- The cost of financing has increased from 7.5% to 11.5%.

- A buyer can only raise $40 million of acquisition financing vs. $60 million in order to maintain an adequate Fixed Charge Coverage Ratio of at least 1.2x.

- A $10 million EBITDA company which was valued at 8.6x just nine months ago may now be worth 6.7x.

| $ in millions | Previous | Current |

| Target EBITDA | $10.0 | $10.0 |

| Leverage Multiple | 6.00x | 4.00x |

| Total Debt | $60.0 | $40.0 |

| Debt % of Total Cap | 70% | 60% |

| Implied Enterprise Value | $85.7 | $66.7 |

| Valuation Multiple | 8.6x | 6.7x |

| 12 Month SOFR | 1.5% | 5.5% |

| Margin | 6.0% | 6.0% |

| Interest Rate | 7.5% | 11.5% |

| EBITDA | $10.0 | $10.0 |

| Less: Management Fees | ($0.3) | ($0.3) |

| Less: Taxes | ($2.0) | ($2.0) |

| Less: CapEx | ($1.5) | ($1.5) |

| Cash Available for Debt Service | $6.2 | $6.2 |

| Cash Interest Expense | $4.5 | $4.6 |

| Amortization | $0.6 | $0.4 |

| Total Debt Service | $5.1 | $5.0 |

| Fixed Charge Coverage Ratio | 1.22x | 1.24x |