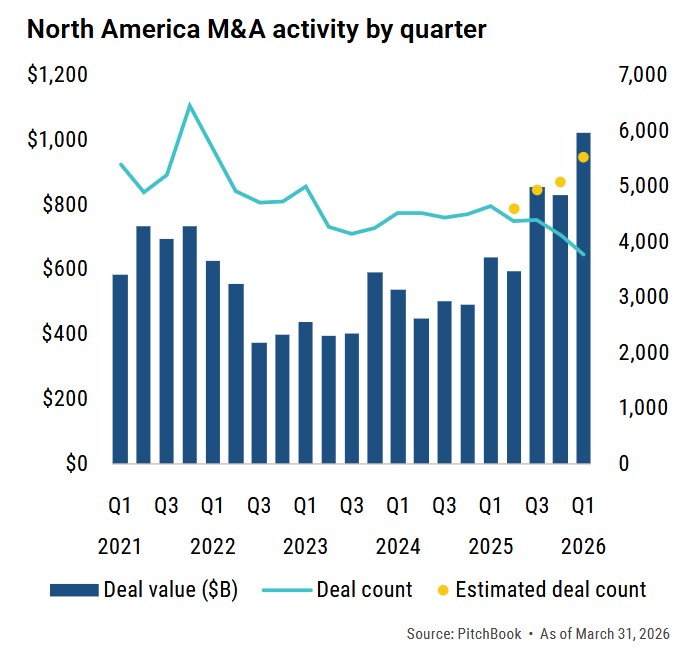

The much-anticipated banner year in middle market M&A is on pause. According to LSEG (as reported by Mergers & Acquisitions), North American middle market deal flow ($100 million to $1 billion in deal size) is down so far in the first two months of this year vs. the first two months of 2024.

While the value of deals is down only 4%, the number of deals is down 18%.

The main issue with the M&A market is uncertainty as it is the public equity market:

· Buyers need certainty or at least clarity in order to aggressively pursue acquisitions if at all.

· Sellers with meaningful exposure to either tariffs or government contracts (which may be impacted by DOGE) therefore are waiting to go to market for the most part (and for good reason).

Not all sectors have been impacted however.

· Domestic services companies (ranging widely from business services to home services to industrial services) have the upper hand. Potential sellers in services with good fundamentals (including ideally recurring contracted revenue) and at least decent financial performance (top-line growth and steady if not improving margins) are now considered scarce assets in middle market M&A and therefore can in many cases demand a premium.

· Domestic manufacturers with little if any reliance on foreign inputs.

· Distributors in sectors ranging from food to industrial products, who tend to be able to pass through price increases almost immediately.

Fingers crossed the tariff situation (including reciprocal and especially retaliatory tariffs) will settle down in the near future and those manufacturers as well as services companies with government contracts get some clarity. Assuming these dynamics transpire within the next few months and the focus from Washington shifts to easing regulation and maintaining if not lowering taxes, the latter part of 2025 should see very strong M&A activity (I know we’ve heard that second half story before). The backlog of deals continues to grow as does the availability of capital.

Check out our Case Studies.