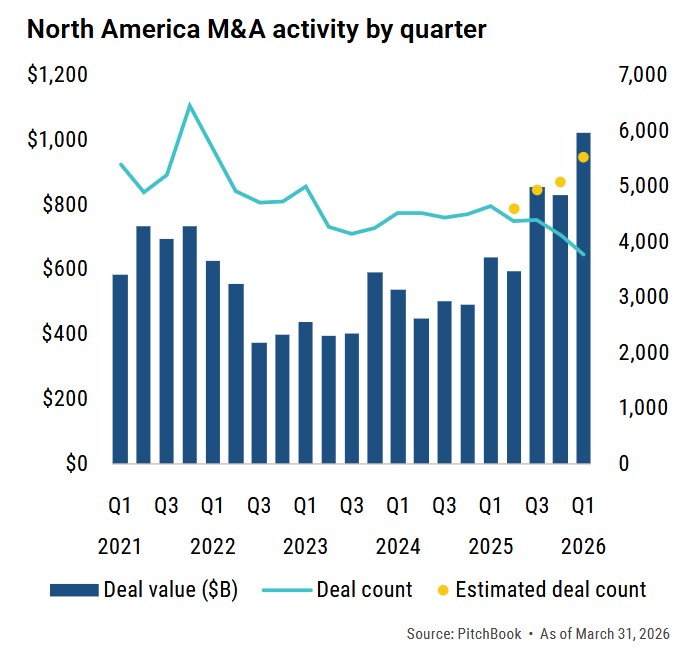

North America M&A Value Up 8% in 2024

According to MergerMarket, although deal count declined, North America M&A value recovered in 2024 rising 8% to $1.7 Tn over 2023, which was the slowest year over the previous 10 years. North America accounted for half of global M&A in 2024 and 9 of the 10 largest deals globally.

Key Drivers of M&A Activity in 2024

- Inflation Moderated

- GDP Growth Remained Solid

- Fed Lowered Interest Rates by 100 bps

- Seller Expectations Finally Began to Adjust

- Significant Buyer Dry Powder While Corporates Maintained an Edge over Financial Buyers

- Millions of Aging Baby Boomers Need Exit Plan

North America M&A by Sector

The strongest sectors were:

- Technology (largest sector): up 27%

- Industrials & Chemicals: up 63%

- Utilities & Energy: up 80%

- Telecom: up 110%

The weakest sectors were:

- Healthcare: down 15%

- Oil & Gas: down 36%

U.S. Private Equity Activity Bounces Back Strongly

2024 was the first up year for U.S. private equity activity since 2021. The value of U.S. private equity transactions increased 19% in 2024 to $839 Bn vs. 2023 while the number of deals increased 13% in 2024 to 8,473.

U.S. Private Equity Exits Increase

The value of U.S. private equity exits increased 50% in 2024 over 2023 to $417 Bn while the number of PE exits increased 17% to 1,502 in 2024.

Add-Ons Continue to Dominate PE Acquisition Activity

Lower mid-market investment banking firms like Calabasas Capital continue to be relatively insulated from macro factors since add-ons are easier to complete and are a priority for platforms to (a) reduce their average buy-in multiples and (b) consistently deploy capital.

In 2024, add-ons represented 74% of all U.S. PE acquisitions (vs. 26% platforms); the number of add-ons completed in 2024 rose 17% vs. 2023 while platforms increased 10%.

Lower Mid-Market Valuations Continue to Bounce Back

According to ACG/GF Data, PE Lower Mid-Market ($1-$250MM in deal size) valuation multiples stabilized in 2024 at an average of 7.1x but remained well below 2021’s peak.

2025 M&A Outlook: Cautiously Optimistic

- No Recession as GDP Growth Remains Solid

- Buyer-Seller Bid-Ask Spread Continues to Narrow

- Continued Availability of Capital

- PE Desperate for Realizations Will Stop Waiting for Higher Valuations

- Millions of Aging Baby Boomers Still Need an Exit Plan

- Much More Favorable Regulatory Environment Expected

- Buyers Have Adapted to Higher Interest Rates

- U.S. remains the most dynamic and productive country in which to invest

- Animal Spirits Rekindled: According to Citizens Bank 2025 M&A Outlook, 54% of buyers surveyed* believe M&A will be strong in 2025, the highest in five years.

BUT…..

- Lower Inflation?

- Tariffs?

- Strong Dollar and Earnings Impact?

2025 Lower Mid-Market M&A Sectors of Focus

These are the sectors we think will be the strongest sectors in 2025:

- Industrial Manufacturing

- strong appetite for quality industrial assets with increased optimism, expected deregulation and pro-business policies

- Domestic Manufacturing, Distribution, Chemicals and A&D

- Business, Industrial and Home Services with Recurring Revenue

- Software/SaaS that incorporates AI & ML and Cybersecurity

- Food Distribution

- Healthcare

- Consumer Products with Diversified Supply Chains