U.S. M&A Activity Rebounds

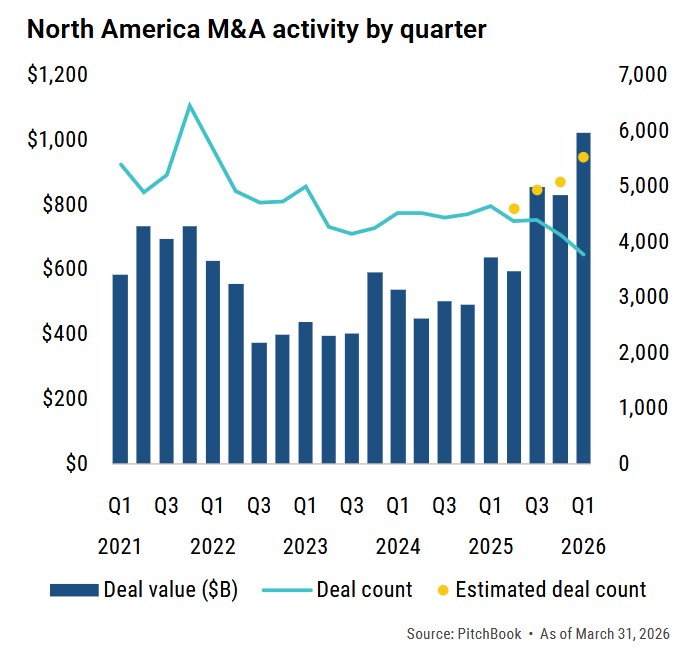

According to EY, U.S. M&A deal activity bounced back strongly in the third quarter of 2025 (3Q25), up 10% sequentially over 2Q25 in terms of number of deals and up 40% sequentially over 2Q25 in terms of deal value as mega deals dominated the landscape.

In September 2025, the M&A market saw an increase in M&A activity and a surge in deal value. Large deals and private equity fueled U.S. deal value. PE played a crucial role in propelling significant US transactions, invigorating both M&A and IPOs through decisive investments and abundant capital. The trend toward large- scale deals accelerated as organizations aimed for greater strategic reach. With market conditions stabilizing, executives expect a busy close to the year, marked by a robust lineup of deals in the pipeline.

U.S. Private Equity Activity Bounces Back

According to Pitchbook, U.S. private equity deal flow in terms of deal count was up sequentially in 3Q25 by 4% as compared to 2Q25 and up year over year by 12% as compared to 3Q24. In terms of deal value, U.S. private equity deal flow was up sequentially in 3Q25 by 28% as compared to 2Q25 and up year over year by 38% as compared to 3Q24 as the average deal value increased in line with overall M&A trends in the quarter.

According to EY, with dry powder at record levels and a more favorable interest rate environment, PE’s share of total U.S. deal value for transactions over $100 million rose to 59.9% in September 2025, up from 44.6% in August 2025, marking a significant shift in market dynamics.

Contributing to strong PE activity has been the availability of capital to finance acquisitions, largely from private credit funds but also more recently again from commercial banks. According to Pitchbook, after hitting a cycle high of 51.1% in 2023 — amid the most aggressive rate hikes in a generation — the average equity contribution to broadly syndicated loan (BSL)-financed LBOs, has eased back to 46% of deal value in 2025. This level is consistent with the 2019-2022 period, based on deals financed through the broadly syndicated loan (BSL) market, and suggests that dealmakers are regaining confidence regarding leverage, even if overall volumes remain muted.

U.S. Private Equity Exit Activity Ramps Up

According to Pitchbook, the number of PE exits in 3Q25 hit its highest mark since the frenzy in 2021 with an estimated 464 exits. This represents a 22% sequential increase in deal count as compared to 2Q25 and an 18% year-over-year increase in deal count as compared to 3Q24.

M&A Market Outlook

Deal momentum remains strong as CEOs prepare for a busy year-end. A significant backlog of transactions is poised to move forward as market conditions stabilize, with pent-up demand expected to drive an uptick in activity. According to the EY-Parthenon report, 48% of CEOs globally plan to pursue more deals, reflecting sustained confidence in acquisitions.

If the Federal Reserve further reduces interest rates in 2025, it could lead to more deal activity in the US due to lower financing costs. However, several factors, such as the federal shutdown, new investigations and unstable tariffs, could complicate the execution of these deals. It is essential for companies to be prepared to plan longer timelines, model scenarios to analyze potential impacts of tariffs and talent costs on operations and deals, and consider structuring agreements to share risks more effectively, which can help maintain certainty in deals and speed up the closing process.