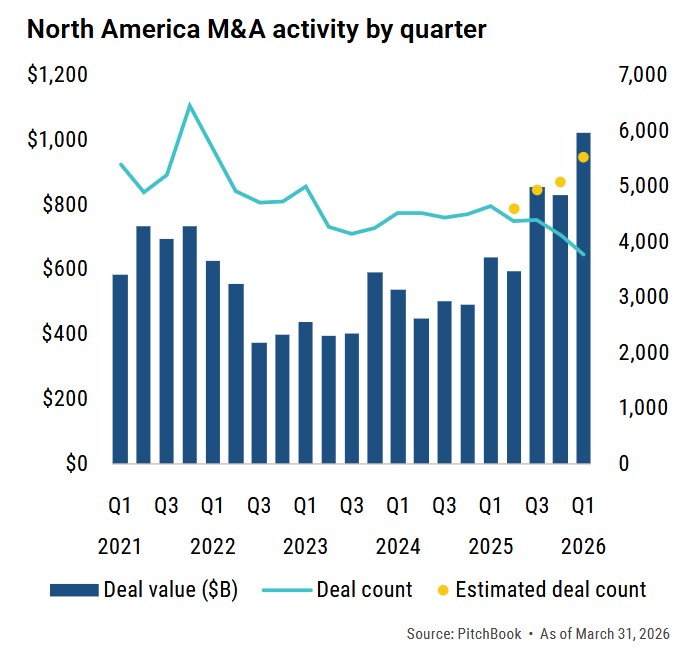

North American M&A Up in 1Q 2026

According to PitchBook, the total value of North American M&A reached a new all-time high of $1,022.2 billion, representing a 23% QoQ increase vs. 4Q 2025 and a 60% increase YoY vs. 1Q 2025. Deal count rose to 5,539, a gain of 10% QoQ and 19% YoY.

There continues to be bifurcation between large and small deals. In 1Q 2026, the 10 largest deals represented about half of the total value of deals, including the largest one which was the $250 billion xAI related party transaction.

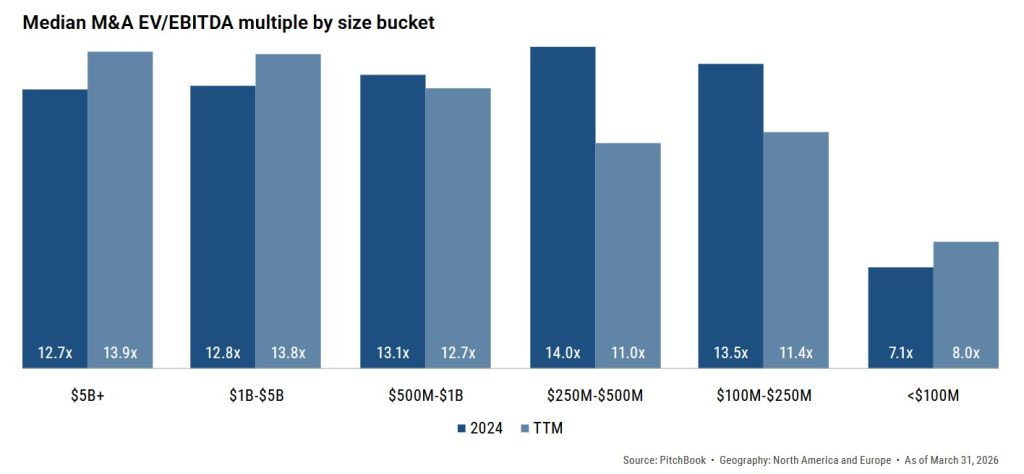

Valuations Still Impacted by Scale

According to PitchBook, on a trailing 12-month (TTM) basis as of March 31, 2026, EBITDA multiples for the largest sized deals (above $5 billion) and the smallest sized deals (less than $100 million) each rose about 10% vs. 2024. The smaller deals continue to be attractive as tuck-in acquisitions. This is also consistent with valuation multiples reported by GF Data, which tracks private equity transactions. GF Data’s contributing private equity firms reported 80 completed transactions during the first quarter at an average valuation of 7.3x TTM adjusted EBITDA. Both readings held above their full-year 2025 levels. Sponsors and corporates are paying up for scale and market leadership.

U.S. Private Equity Deal Value Down

While the number of U.S. private equity transactions closed in 1Q 2026 of 2,415 was up 5% QoQ and 6% YoY, the value of $260.2 billion (including estimates for late-reporting and undisclosed values), represented a decline of 18% QoQ and a decline of 7% YoY. This demonstrates how PE buyers have moved down-market to smaller deals.

U.S. Private Equity Exits Way Down

According to PitchBook, the value of PE exits in 1Q 2026 was down 33% QoQ compared to 4Q 2025 and down 35% YoY vs. 1Q 2025. Similar to 2025 when ‘Liberation Day’ put the brakes on a promising year, the start of 2026 has faced unexpected headwinds, AI disruption, the war in Iran, and reduced odds of rate cuts. Nevertheless, exit activity in 1Q 2026 remained resilient, as the QoQ and YoY declines were exacerbated by the relative outperformance in exits in the comparable quarters of 1Q 2025 and 4Q 2025 as demonstrated by the chart.

M&A Market Outlook

Dealmakers continue to race to close deals as geopolitical risks spike, and inflation remains stubbornly high leading to expectations of a rate increase this year as opposed to further rate cuts. Adding in the concern of an AI-induced ‘SaaS-pocalypse’, we are faced with lower activity in middle market M&A so far in 2026.

The theme we’ve seen play out over the past two years, therefore, continues today. Mega deals continue to close as do small strategic add-ons. The upper middle market, however, where sellers (including PE owners) are still reluctant to sell at current valuations.